In

the recent months, the macroeconomic environment has been stormy. Global

conditions have caused structural breaks in risk perception and appetites which

have contributed to a significant rebalancing of Indian portfolios. This

has further led to increased volatility and instability in currency and capital

markets. The decelerating domestic growth and persistent inflation and

upside pressure of a depreciating rupee worries all and sundry. However, even

though the overall macroeconomic conditions look worrisome we must take a

forward-looking view of the policy responses and its consequences on indicators

and future risk.

Over

the past two years, the performance of major advanced macro- economies has

raised concerns over the sustainability of global revival. On the contrary,

emerging economies have exhibited reasonable growth, suggesting that their

domestic drivers and increased linkages with each other and the advanced

economies have facilitated their growth stories. However, these growth stories

have been curtailed by slower growth in advanced economies, sovereign debt

pressure from Europe and growth volatility in US. The European debt

problem has without a doubt been the overriding global factor in recent months

triggering confidence problem and volatility in currency and capital markets

across the globe. As the prospects of any solution have ebbed and flowed, so

have the asset prices and exchange rates. It was expected that a solution would

come out from the crucial December Euro Summit or the recent ECB meeting in

January; however these expectations are still to be realized.

The

impact of the brewing global instability on India has been enormous. An

emerging economy is structurally current account deficit and so is India. This

deficit is usually financed by capital inflows, which over the past decade has

been stable and large in magnitude and hence had more than offset the current

account deficits. However, in the recent months there has been a significant

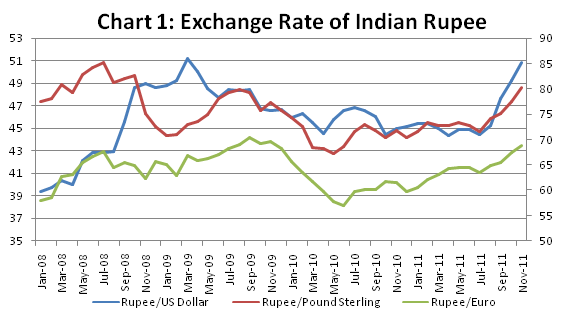

reversal and the observed effects are much like the 2008-09 global

financial crisis (Chart 1). Between July 2008 and February 2009, the Rupee

depreciated by nearly 17 percent. This happened because of lack of

capital inflow, which resulted in the current account driving the exchange rate

and naturally, this pressure resulted in Rupee depreciation.

{kind=link}

For the past few years, the Indian exchange rate regime has been

described as ‘bounded float’. Fundamentally, there is no restriction on Foreign

Direct Investment (FDI), except for limits on specific sectors and portfolio

investment in equities. However, there are restrictions on debt inflows

due to external stability issues. In particular, these limits relate to

quantity, tenor and pricing. Short-term debt is most vulnerable to sudden reversals

and hence it’s least preferred; while long-term debt is viewed more favorably

as it is seen as a resource channel for inflow into infrastructure despite the

associated risk concerns. These debt controls may be viewed as ‘strategic’

capital controls; they are altered infrequently in response to macroeconomic

conditions. However, these and other capital account management tools are

used to help in bounded float when volatility increases. The exchange

rate is determined by daily variations in demand and supply and hence a sharp

fall in capital inflows leads to a situation of excess demand leading to

exchange rate depreciation.

In times of bountiful capital inflows, current account surplus

economies build up their foreign exchange reserves, which may be utilized in

troubled times to manage exchange rates and meet short-term claims without

disruptions or loss of confidence. India has reserves over $300 billion, but

because of current account deficit, the reserves are essentially

counter-balanced against our external liability position. The recent

depreciation did not witness radical utilization of this foreign exchange

reserves due to our current account deficit but also because excessive

utilization of reserves could have resulted in deterioration of confidence in

the economy’s ability to meet short term obligations. Alternately, if foreign

exchange reserves were not utilized exchange rates could spiral out of control,

triggered by self-fulfilling expectations. Hence, it was necessary to strike a

balance.

The Reserve Bank of India (RBI) struck this balance by structural

capital controls. In particular, they increased foreign currency supply by

expanding market participation. This was done by increasing the investment

limit in government and corporate debt instruments by foreign investors,

raising interest rate ceilings payable on non-resident deposits and enhancement

of the all-in-cost ceiling for external commercial borrowing. In addition, RBI

undertook administrative measures to curtail the temptation of market

participants to take positions against Rupee. For instance, entities which

borrow abroad were now required to use a portion of their fund for domestic

expenditure immediately. These measures facilitate a balance between short-term

risk of Rupee spiraling downwards and the medium-term risk of a loss of

confidence in India’s ability to meet external obligations.

Domestic Liquidity state

The domestic liquidity condition has come to fore-front since the

borrowing under Liquidity Adjustment Facility (LAF) has been above the one

percent of Net Demand and Time Liabilities (NDTL) threshold. The RBI makes a

distinction between the monetary stance and liquidity stance and exploits this

distinction by carrying out Open Market Operations (OMO’s) to inject liquidity

into the system, despite maintaining an anti-inflationary monetary stance. The

RBI did this form of intervention in December 2010 and November

2011.

In spite of the OMO and advance tax payments in mid-December,

domestic liquidity conditions are still expected to remain stretched for some

time. Still, RBI must be careful that OMOs and LAF intervention do not result

in excessive accommodation but ensures adequate liquidity (consistent with the

comfort levels).

In this regard, RBI has a wide range of instruments which have

been utilized. For instances, the banking system as a whole hold 29 percent of

NDTL as opposed to the stipulated Statutory Liquidity Ratio (SLR) of 24

percent . Thus as and when the need arises a liquidity infusion of 2,740

billion is plausible. However, we cannot rely on this entirely as SLR

default is a serious offence for large banks and most banks life keeping the

Liquidity in excess of SLR stipulation to avoid default. Alongside this lies

the recently established Marginal Standing Facility (MSF) which allows banks to

use a further one percent of SLR holdings. However, banks would exploit this

only in situations of extreme stress. In recent weeks there hasn’t been any

recourse to this window which could indicate that there isn’t much stress,

however stress is brewing and we must be cautious. Furthermore, we must keep in

mind that the large fiscal deficit cannot be fully accommodated by OMO’s and

hence we must manage domestic liquidity condtions such that they do not

de-stabilize financial markets and that too without violating the current

monetary policy stance. However, an inadequate response can weaken our monetary

control and also effect medium term inflation expectations.

Growth and Inflation Puzzle

Growth and Inflation are the two most commonly discussed phrases

and the cornerstones of any form of macroeconomic development. Anything and

everything has some impact on these two macroeconomic indicators. They also

take us from the immediate worries to futuristic troubled waters. Since the

last quarterly review by RBI a lot has happened to Rupee and inflation. The

headline inflation clocked a two year low at 7.47 percent in December 2011. It

stood at 9.11 percent in November 2011 and it is believed that the decline was

prompted by cheaper food items. Commodity prices have softened to a large

extent. Fuel and power segment inflation stood at 14.91 percent on an annual

basis in December as opposed to 15.48 in November. Furthermore, stable crude

oil prices in dollar terms favored the domestic inflation in December in-spite

of depreciation in Rupee. Any positive news from European sovereign debt

problem would also moderate the inflation risk, however the likelihood of such

positivity in the near vicinity is bleak.

The Quarterly estimates of Q2 of 2011-12 substantiate the growth

moderation story some of it is attributable to external macroeconomic events

and interest rate hikes. RBI intervention of increasing interest rates to

curb inflation has moderated demand as growth deceleration precedes inflation

deceleration. If the current deceleration in inflation level continues in

the coming months, RBI policy stance would be receiving accolades. However, the

growth deceleration is also driven by the global turbulence and an investment

lull. The government is initiating a number of reforms (tax reforms, skill

formation, increased transparency in the system) to facilitate our growth

stories. However, quick resolution and implementation is a key to success.

Even though food price inflation has been on a steady decline it

is still a worrisome risk factor. It would persist to be a source of

inflationary pressure unless there is radical improvement in technology driven

productivity, both at the cultivation stage and more importantly at the

distribution and procurement stages. This would require many multilateral

forces to come into action, such as infrastructure, technology, market

institution reforms, price incentive realignment and the financial services

that can support the realignment. However, these must be brought in rather

quickly to achieve the target.

In conclusion, we need to balance the risk of rupee spiral and

loss of confidence in Indian economy in the short term. It should be understood

that the volatility and liquidity stress would last a while and prudent

management of capital accounts and liquidity is essential to tide the worrisome

waves. The good news is that the growth-inflation dynamics is manageable

and the coming year looks brighter than the year gone by. However, long term

growth does require structural policy change at a rapid pace.

No comments:

Post a Comment